Non-QM hedging advisory services

The industry has seen non-QM lending explode over the past few years and the government’s drive to see more affordable lending could lead more lenders to consider offering these products. That said, not all non-QM loan products are aimed at low-income borrowers.

In truth, the non-QM category covers a wide range of mortgage loan products, which may explain why there are so few companies that have developed a good methodology for valuing them and hedging against changes in the value of these assets. Even though these products are priced to consumers at a premium, every lender builds additional margin into their loan pricing to hedge against interest rate risk. It can be a very profitable business, but incorrect hedging can lead to serious problems.

Non-QM borrowers tend to respond to interest rate changes and changes in their credit, which can create a great deal of volatility in the lender’s pipeline. Because most JUMBO loans are non-QM, high balance deals, the lender’s pipeline can grow rapidly. A single loan falling out can mean millions of dollars in difference when it comes time to sell monthly production into the secondary market.

Without good pipeline hedging, this business can be difficult or impossible to manage correctly. Selling another deal may seem like an effective hedge, but it’s not dependable, especially in a rising rate environment. Many non-QM lenders will sell off their production immediately, getting the best execution they can at the time. With the right hedging strategy and better insight into investor pricing, lenders can create bulk sales and get higher pricing with a mandatory delivery. The pricing differential between best efforts delivery and mandatory delivery is substantial on the non-QM side.

The same concerns impact correspondent lenders who make a business of aggregating these loans. It’s very important that they hedge against loss in their pipelines.

MCM has been hedging non-QM pipelines and servicing portfolios for existing customers for over a year. Our advice to lenders who offer these products is not to hedge at their own peril. There is already enough credit risk in these deals, which can be hedged by purchasing a CDO. This is less of a problem if the lender does a very good job of hedging against interest rate risk.

But there is no simple solution for most lenders. They don’t have access to the information or the analytical software that MCM brings to the task. As interest rates rise, the yields on non-QM products rise as well, which drives the pricing lenders can get on the sale of these assets down. Lenders can hedge against this and MCM can help.

One common mistake we’ve seen is lenders hedging against non-QM interest rate risk by buying three- and five-year Treasury swaps. In our experience, that just introduces more basis risk. It’s better to hedge with premium 15-year mortgage backed securities, which gets the lender close to the same point duration and convexity that they have from their non-QM products.

Each lender runs their business differently and an actual hedging strategy will depend upon a number of factors. It requires answers to the right questions.

Partnership Account

MCM advises clients, who then execute trades, best execution based pooling and delivery. MCM is always available for conference calls to discuss trading strategies and to provide consulting and market analysis.

Guardian Account

MCM does it all, executing MBS trades, providing best execution based pooling and delivery, monitoring pricing and leading a daily client conference call to coordinate secondary marketing activities.

In both cases, our services keep pace with our client’s efforts, providing continuous support and advice from expert MCM Advisors. Further, our advice is not generic, but rather tailored to the specific needs of our clients.

Since 1994, Mortgage Capital Management has helped mortgage bankers of every size become more profitable through the use of best-in-class pipeline risk management tools and strategies. Our pipeline risk management services, secondary marketing consulting, and hedging/trading services enable clients to prosper in any market environment.

For nearly 30 years, the U.S. mortgage industry has called upon Mortgage Capital Management for expert advice and proven technologies all designed to deliver best execution in service to a more profitable enterprise. Our customer list includes some of the most successful firms in the business.

Viewing the online demo costs you nothing and will shed light on a unique approach to secondary marketing success that you won’t find anywhere else. Don’t settle for mediocre results for your Non-QM lending business when excellence is achievable.

Get the MCM Competitive Advantage! Call us to today to learn more or schedule an online demo: 858.483.4404 x220

Call us to today to learn more or schedule an online demo

Project & Services

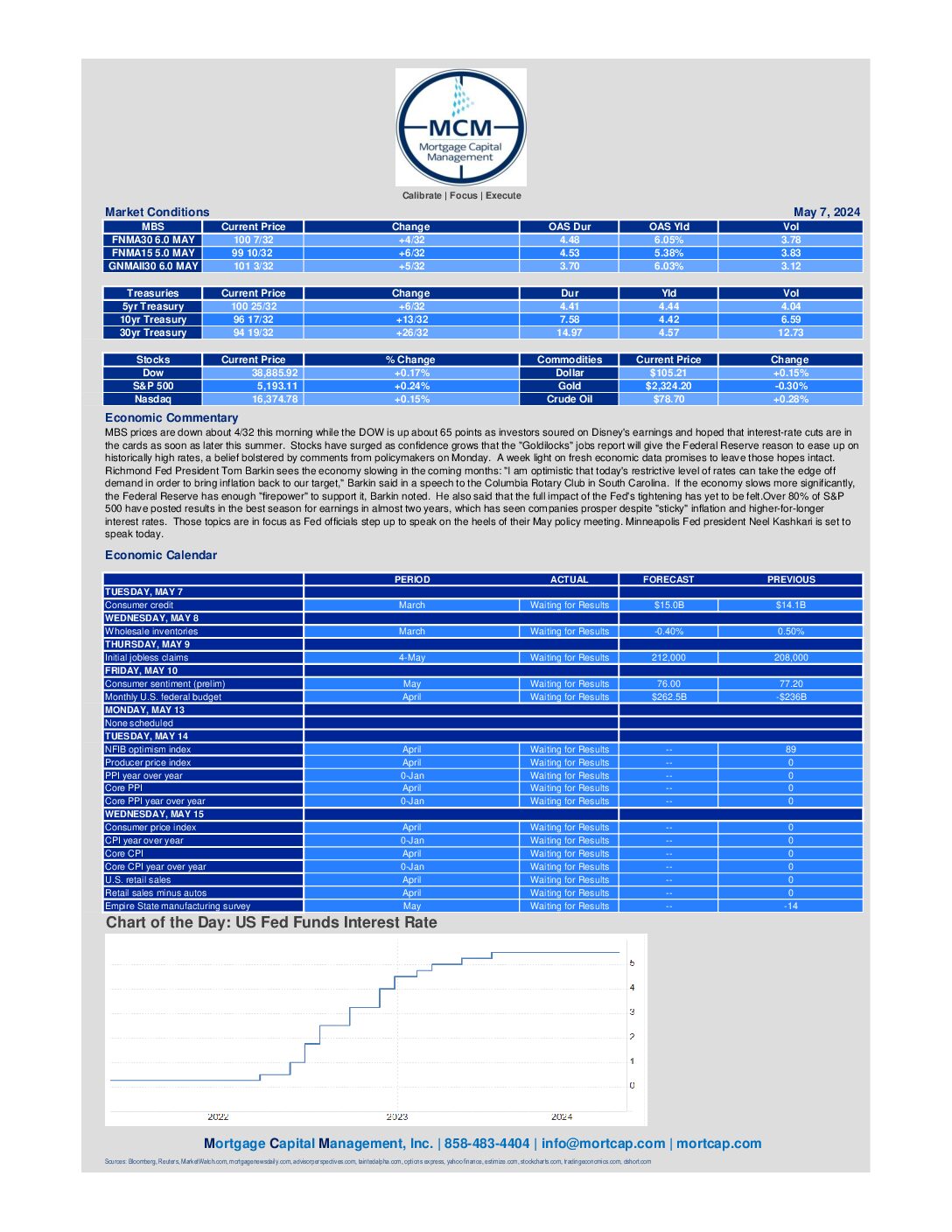

May 7th Market Commentary

MBS prices are down about 4/32 this morning while the DOW is up about 65 points as investors soured on Disney's earnings and hoped that interest-rate cuts are in the cards as soon as later this summer. Richmond Fed President Tom Barkin sees the economy slowing in the coming

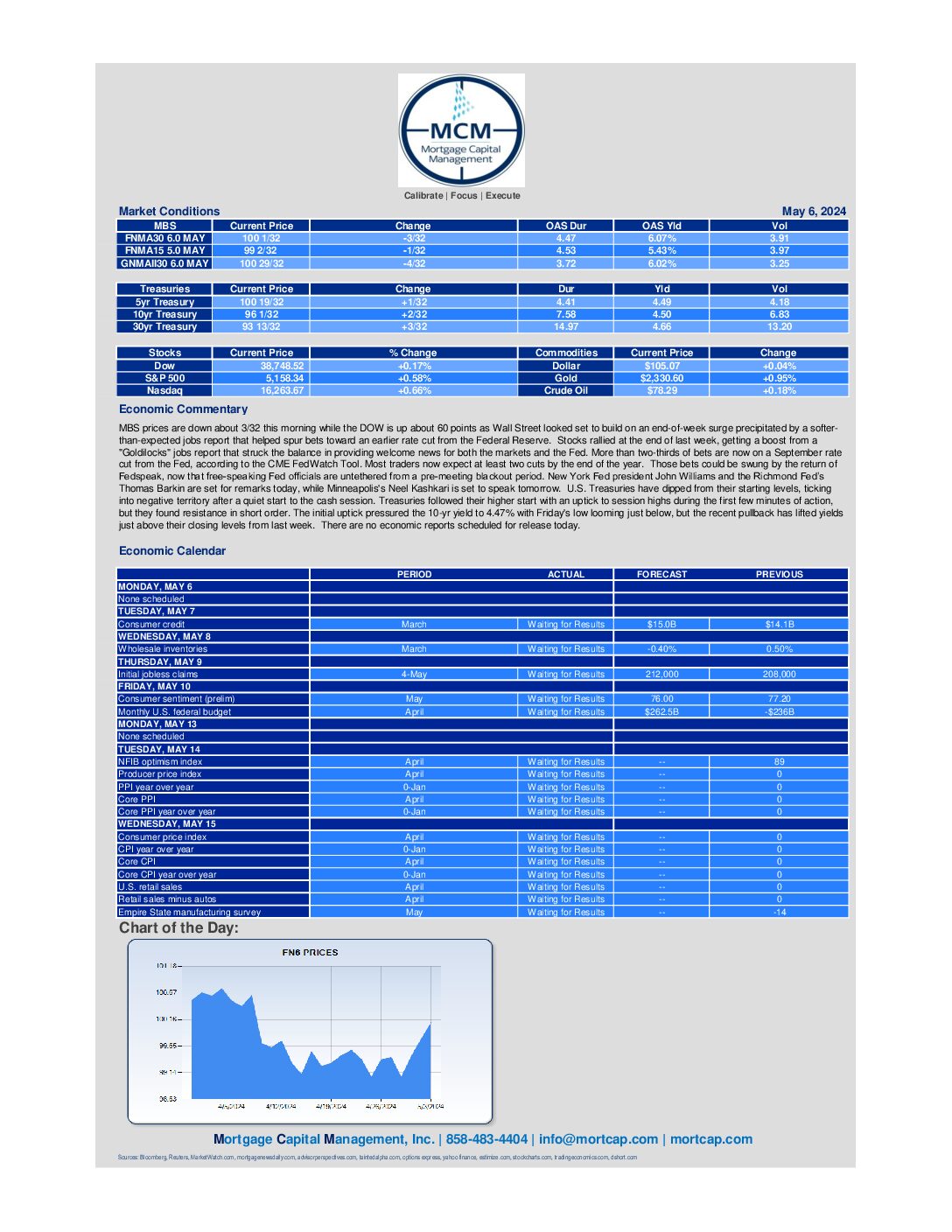

May 6th Market Commentary

MBS prices are down about 3/32 this morning while the DOW is up about 60 points as Wall Street looked set to build on an end-of-week surge precipitated by a softer-than-expected jobs report that helped spur bets toward an earlier rate cut from the Federal Reserve. More than two-thirds

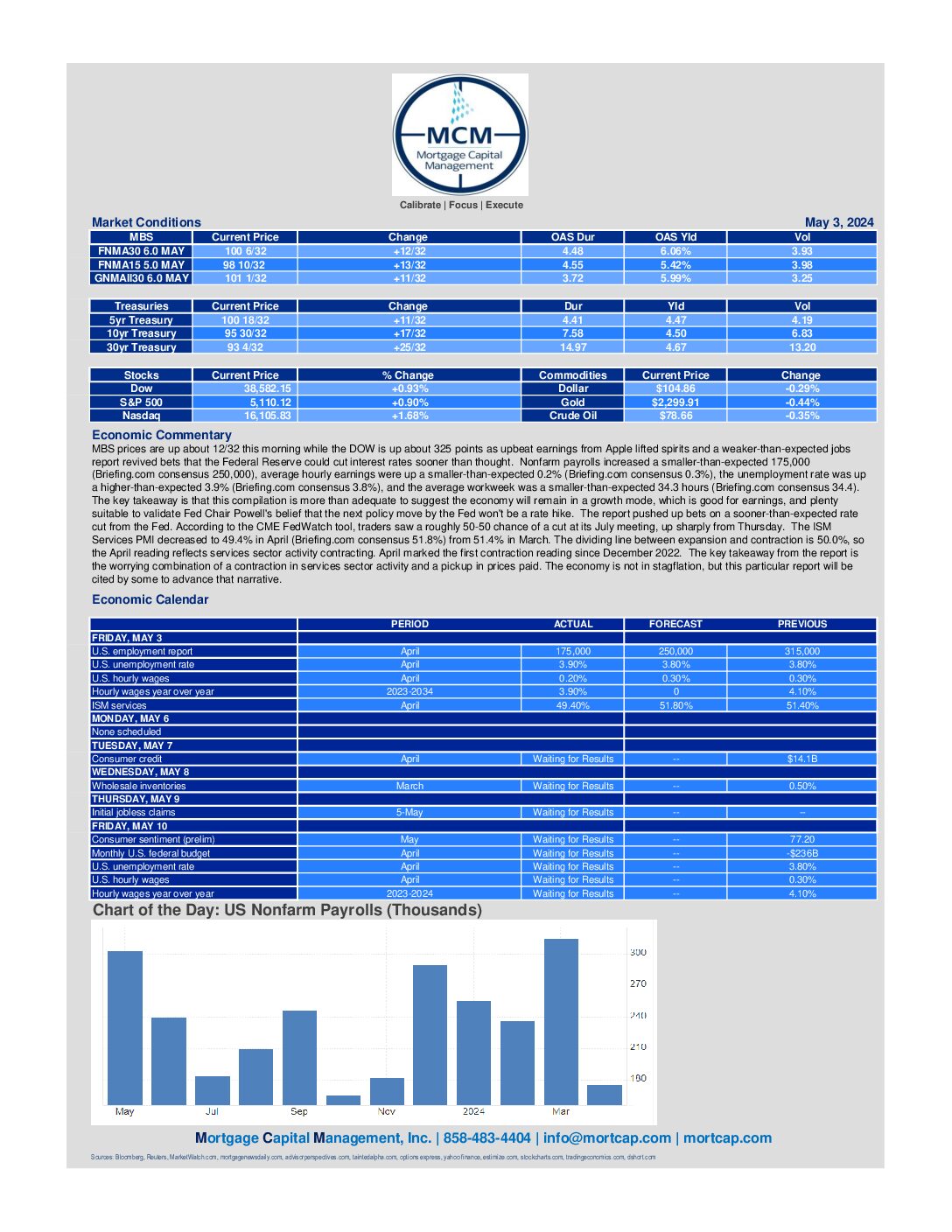

May 3rd Market Commentary

MBS prices are up about 12/32 this morning while the DOW is up about 325 points as upbeat earnings from Apple lifted spirits and a weaker-than-expected jobs report revived bets that the Federal Reserve could cut interest rates sooner than thought. Nonfarm payrolls increased a smaller-than-expected 175,000 (Briefing.com consensus

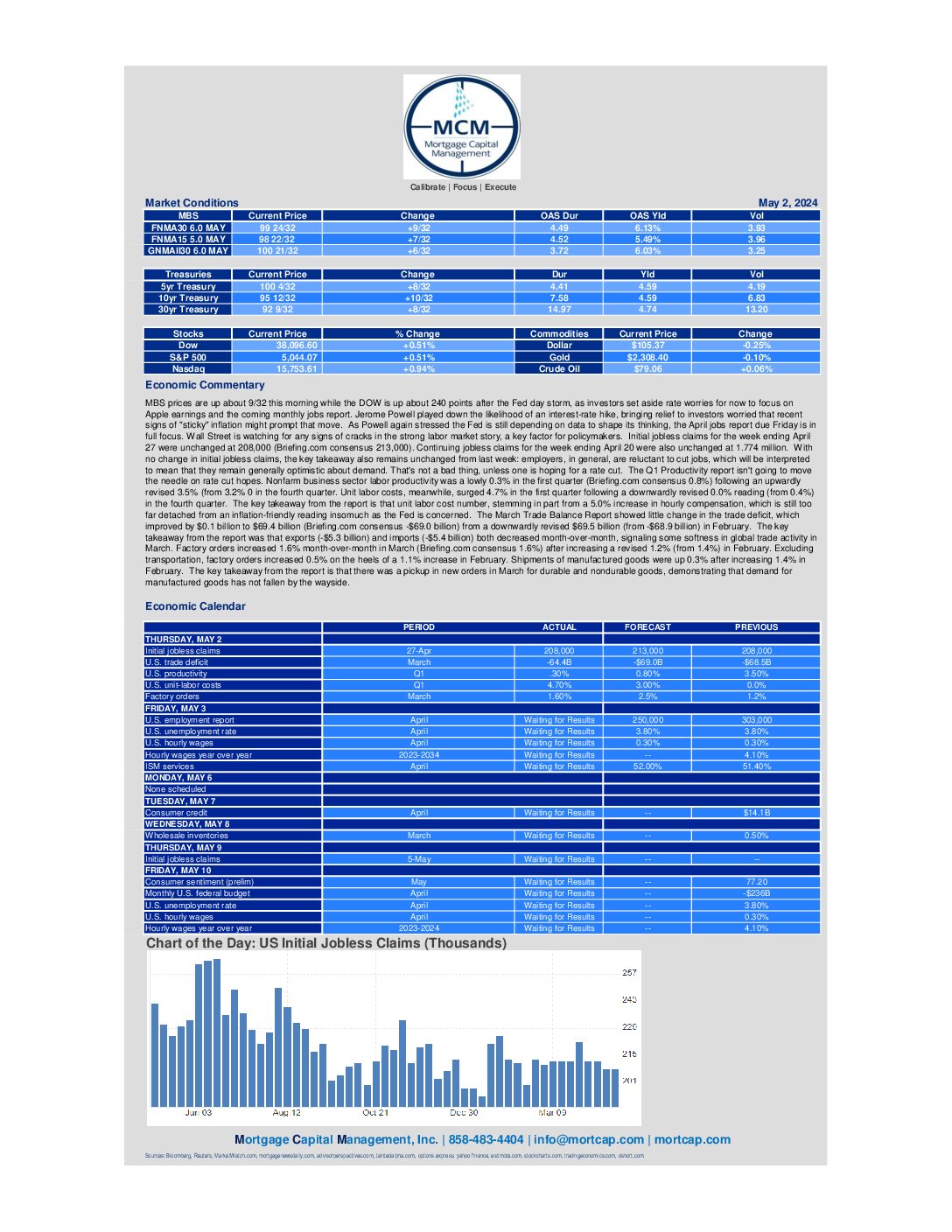

May 2nd Market Commentary

BS prices are up about 9/32 this morning while the DOW is up about 240 points after the Fed day storm, as investors set aside rate worries for now to focus on Apple earnings and the coming monthly jobs report. Jerome Powell played down the likelihood of an interest-rate hike,

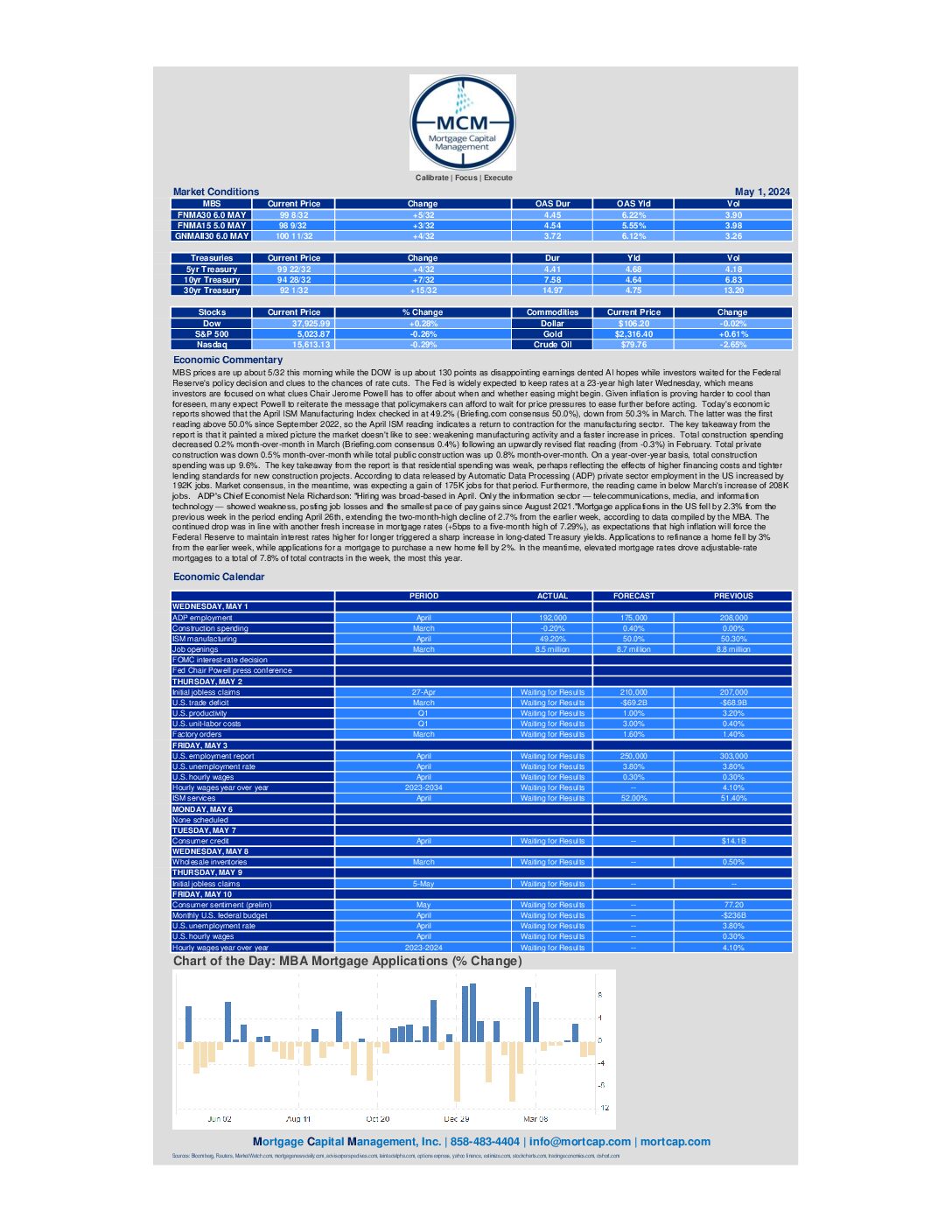

May 1st Market Commentary

MBS prices are up about 5/32 this morning while the DOW is up about 130 points as disappointing earnings dented AI hopes while investors waited for the Federal Reserve's policy decision and clues to the chances of rate cuts. The Fed is widely expected to keep rates at a

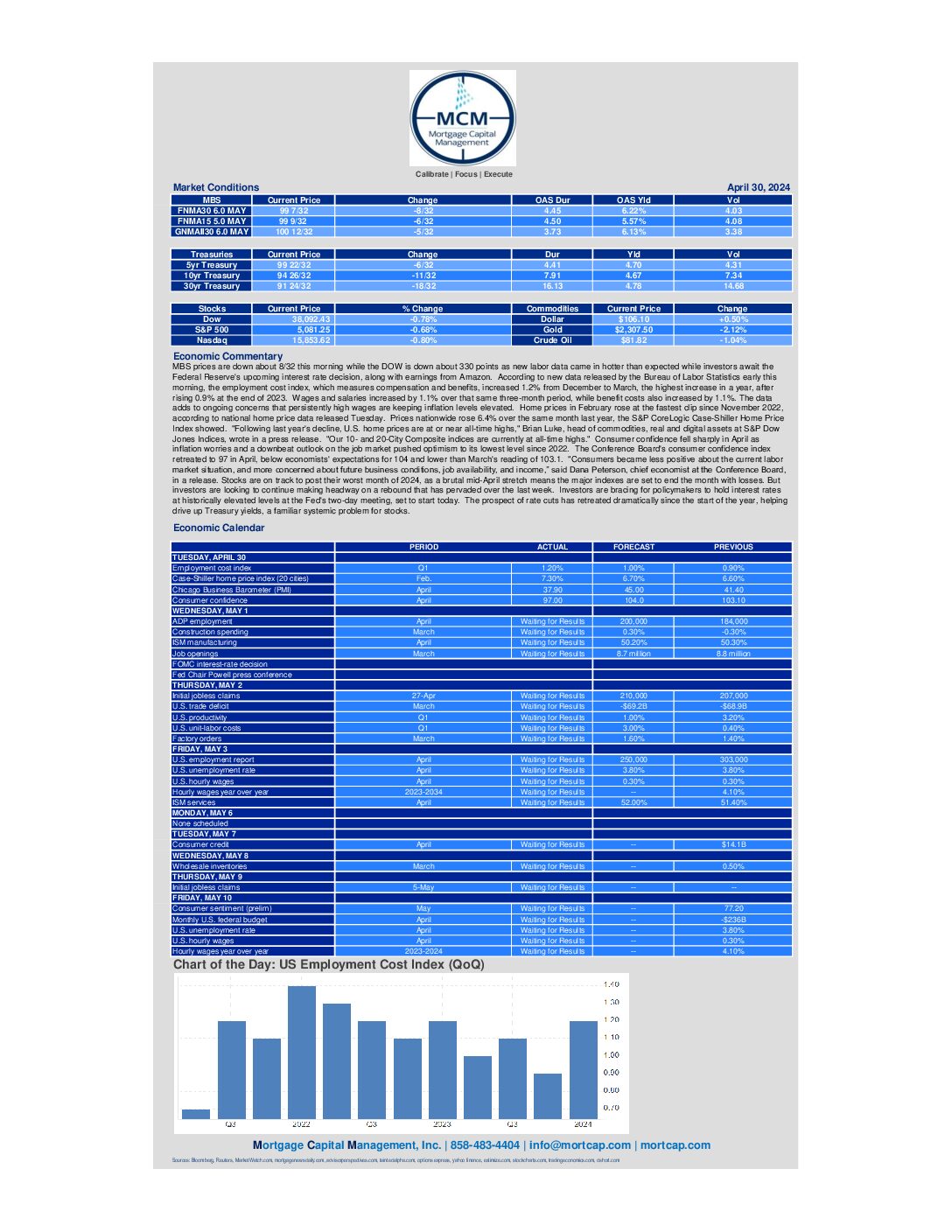

April 30th Market Commentary

MBS prices are down about 8/32 this morning while the DOW is down about 330 points as new labor data came in hotter than expected while investors await the Federal Reserve's upcoming interest rate decision, along with earnings from Amazon. Investors are bracing for policymakers to hold interest

April 29th Market Commentary

MBS prices are up about 4/32 this morning while the DOW is up about 110 points to start a big week filled with a Federal Reserve rate decision, the monthly jobs report, and earnings from more "Magnificent Seven" tech heavyweights. In focus is whether Fed policymakers will backtrack

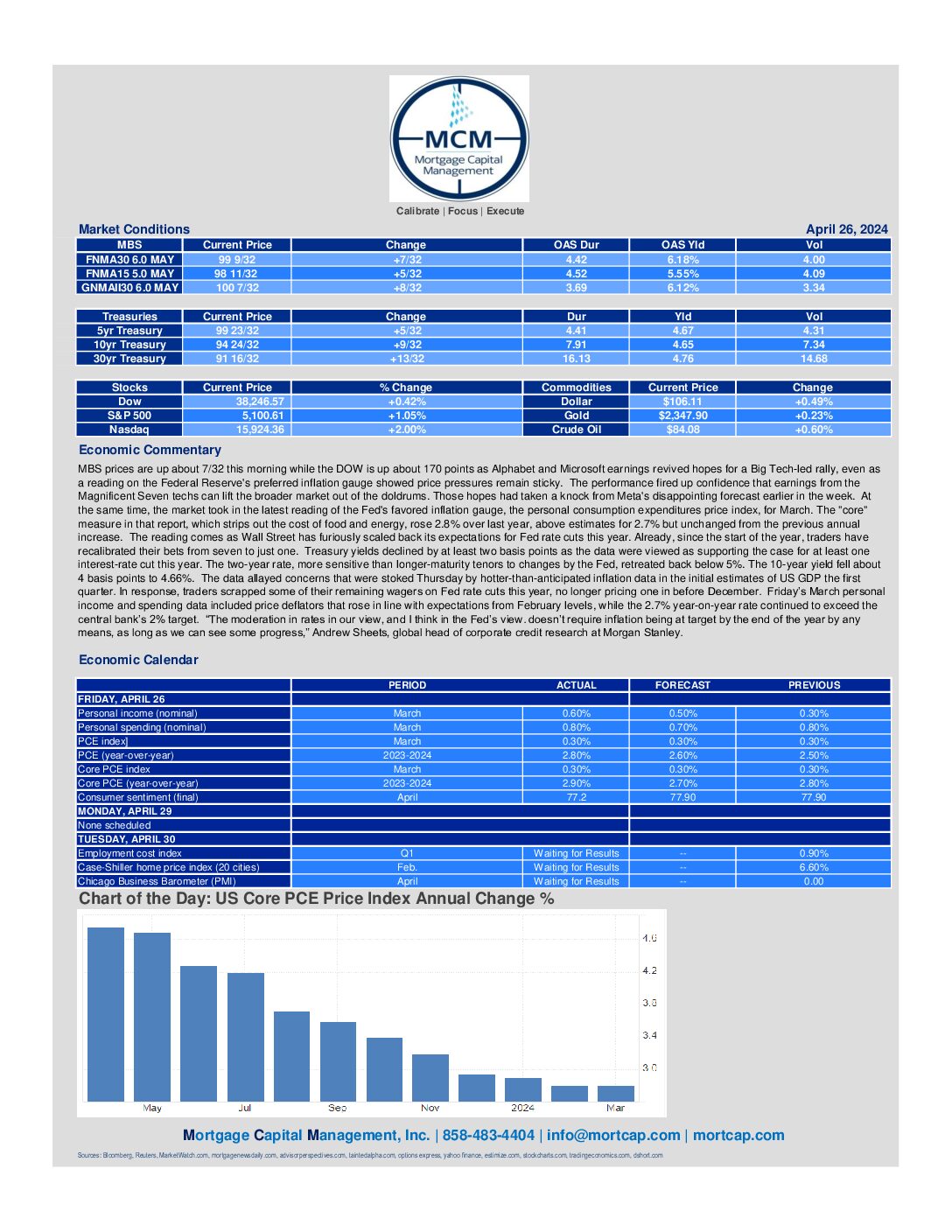

April 26th Market Commentary

MBS prices are up about 7/32 this morning while the DOW is up about 170 points as Alphabet and Microsoft earnings revived hopes for a Big Tech-led rally, even as a reading on the Federal Reserve's preferred inflation gauge showed price pressures remain sticky. Treasury yields declined by

April 24th Market Commentary

MBS prices are down about 7/32 this morning while the DOW is down about 130 points as the ten year treasury yield rose 1.17% to 4.65. Mortgage applications in the US fell by 2.7% from the previous week in the period ending April 19th, trimming the 3.3% increase

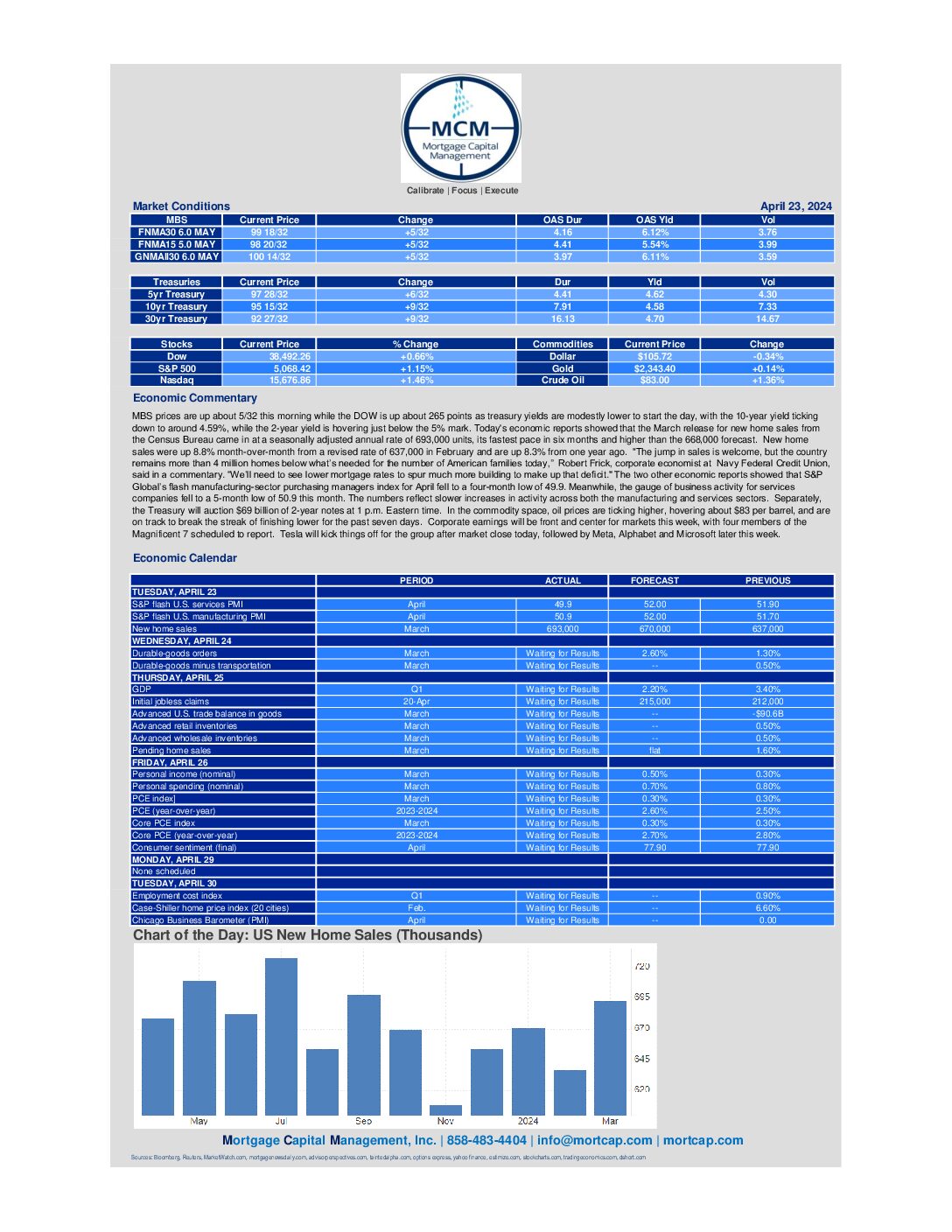

April 23rd Market Commentary

MBS prices are up about 5/32 this morning while the DOW is up about 265 points as treasury yields are modestly lower to start the day, with the 10-year yield ticking down to around 4.59%, while the 2-year yield is hovering just below the 5% mark. Today's economic reports showed