OAS Servicing Valuations

You cannot achieve best execution for your secondary market trades if you don’t take into account the value of the servicing asset. In some cases, it makes sense to retain these assets. In others, a better outcome can be achieved by selling them off. While very few of our clients come to us only to put a value on these assets, we have done that in the past.

It’s more common for us to provide our valuation expertise as part of a larger engagement. For instance, many of our clients execute trades but retain the servicing. While our primary business has long been providing best execution trades into the secondary market, it’s important for our clients who retain their servicing to know the value of these assets. As a result, we have built a successful business performing Option-Adjusting Pricing for Mortgage Servicing Rights.

This is an important part of the total sale optimization offering that MCM makes available because there are circumstances where it makes sense to sell off the servicing. To make that determination, we have developed an expertise at evaluating these assets.

Unlike most companies that evaluate these assets, we don’t rely on a cash flow model. We use the OAS valuation methodology. This takes into account many factors, including the type of loan, the loan amount, the intent, the purpose, the location, and other factors that can impact the value. We then test these values by performing what-if analysis, shocking interest rates up and down and using the client’s cost of funds and their return requirements as part of the valuation metric.

This method is much more accurate and can be customized to the specifics of the lender, which provides advantages that other methods do not. We don’t just answer the question, “What is the value of the servicing for this loan to the market?” We answer the question, “What is this loan’s servicing worth to you?”

We don’t go into the market in search of similar portfolios to give our clients an estimate of the value in their own portfolio. We actually do a loan level analysis of our clients’ portfolios.

This is a very complex analysis that requires us to know our client’s earnings goal, consider the spread between that amount and that the market is currently offering, factor in the yield curve and consider the duration of the assets. We evaluate every loan in the portfolio individually and then combine the results to value our client’s servicing portfolio.

Our clients have a much better idea of the value of their business and can make better decisions about the execution of future loan production. And when it comes to selling their existing servicing rights, they know exactly what these assets are worth to them, so they never have to settle for selling for less.

When it comes to hedging strategy, having this kind of valuation on their servicing is very valuable, especially in an environment where interest rates are rising and lenders need to hedge long term locks and float down locks.

MCM provides this service to clients working with us through either type of relationship:

Partnership Account

MCM advises clients, who then execute trades, best execution based pooling and delivery. MCM is always available for conference calls to discuss trading strategies and to provide consulting and market analysis.

Guardian Account

MCM does it all, executing MBS trades, providing best execution based pooling and delivery, monitoring pricing and leading a daily client conference call to coordinate secondary marketing activities

Under either type of business relationship, MCM’s systems, reporting and analysis tools are all available online providing instant accessibility to comprehensive analysis and reports, eliminating the need for the client to load, maintain and manage the software.

Ease of access, ease of use, quick report generation and real‑time “what‑if” scenarios all provide the client with the necessary tools to succeed in the world of risk management. Combined with MCM’s experienced advisors, Hedge Commander allows clients to grow and prosper in any market environment.

Since 1994, Mortgage Capital Management has helped mortgage bankers of every size become more profitable through the use of best-in-class pipeline risk management tools and strategies. Our pipeline risk management services, secondary marketing consulting, and hedging/trading services enable clients to prosper in any market environment.

For nearly 30 years, the U.S. mortgage industry has called upon Mortgage Capital Management for expert advice and proven technologies all designed to deliver best execution in service to a more profitable enterprise. Our customer list includes some of the most successful firms in the business.

Viewing the online demo costs you nothing and will shed light on a unique approach to secondary marketing success that you won’t find anywhere else.

We’re also open to discussing your unique requirements to arrive at a workable solution that will help you achieve your unique goals. Once you see what’s possible with modern financial services technology, your successful future will begin to come into focus. Don’t settle for mediocre when excellence is achievable.

Get the MCM Competitive Advantage! Call us to today to learn more or schedule an online demo: 858.483.4404 x220

Call us to today to learn more or schedule an online demo

Project & Services

May 8th Market Commentary

MBS prices are down about 3/32 this morning while the DOW is up about 85 points as investors tried to read the rate-cut runes and weighed a fresh batch of earnings reports for insight into the chance of a corporate America-spurred revival. Mortgage applications in the US rose

May 7th Market Commentary

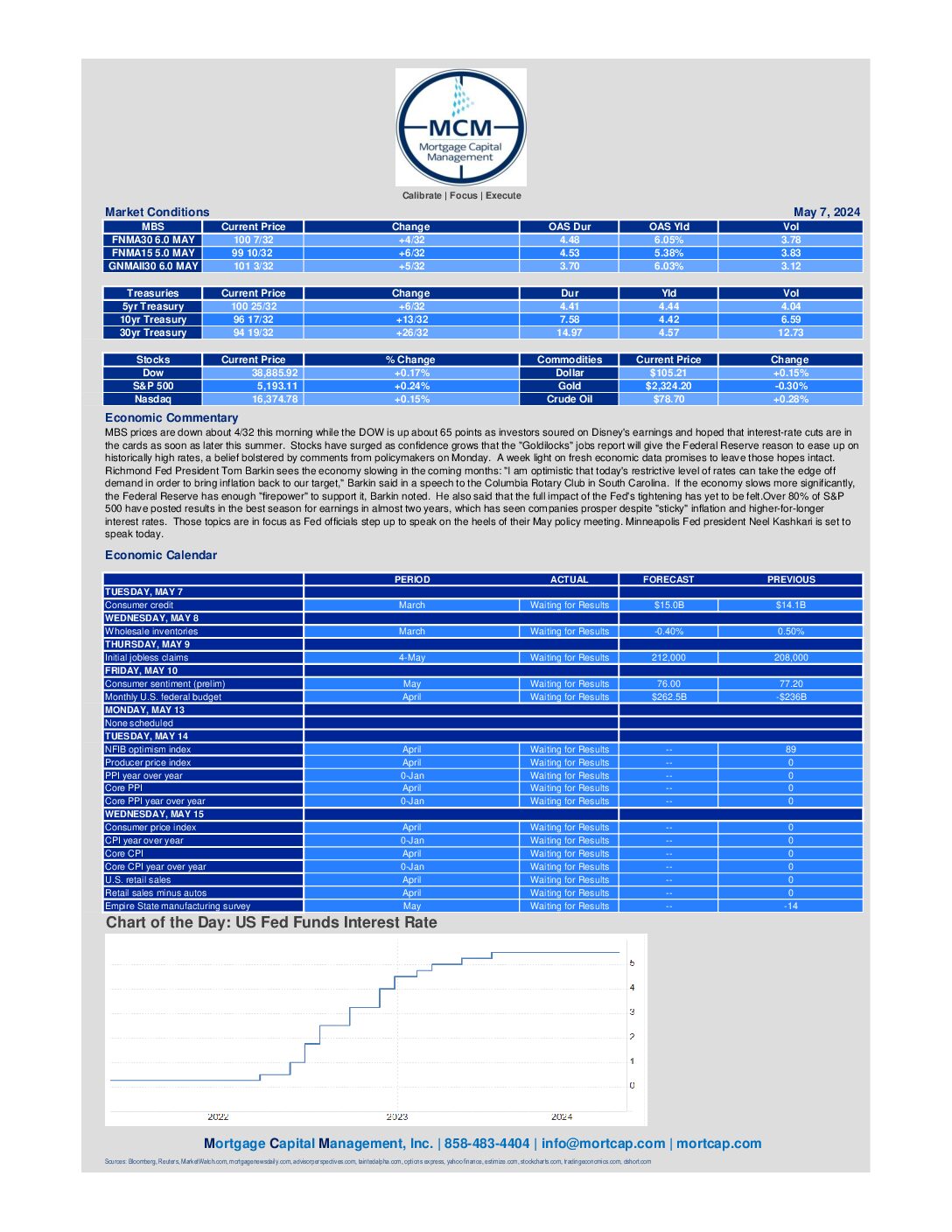

MBS prices are down about 4/32 this morning while the DOW is up about 65 points as investors soured on Disney's earnings and hoped that interest-rate cuts are in the cards as soon as later this summer. Richmond Fed President Tom Barkin sees the economy slowing in the coming

May 6th Market Commentary

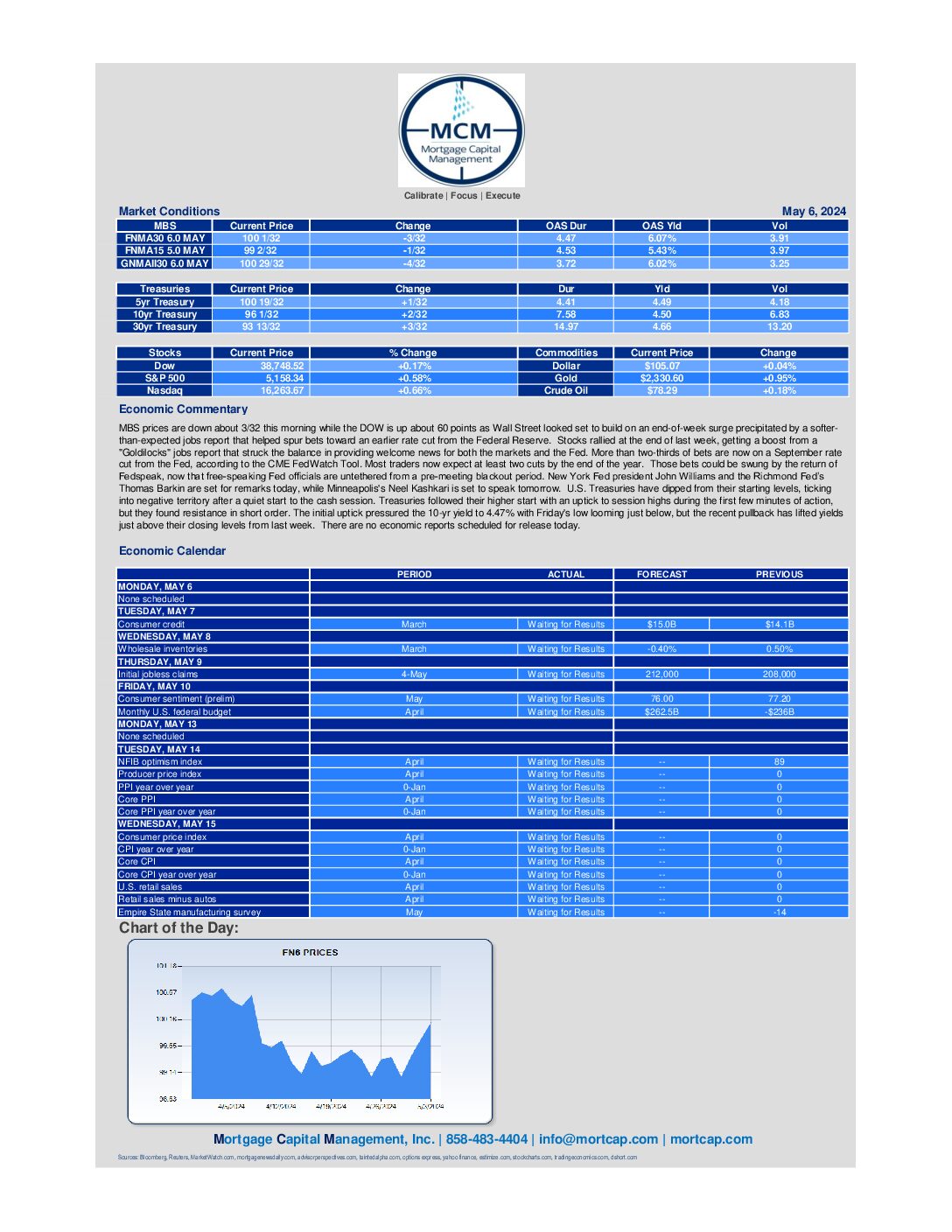

MBS prices are down about 3/32 this morning while the DOW is up about 60 points as Wall Street looked set to build on an end-of-week surge precipitated by a softer-than-expected jobs report that helped spur bets toward an earlier rate cut from the Federal Reserve. More than two-thirds

May 3rd Market Commentary

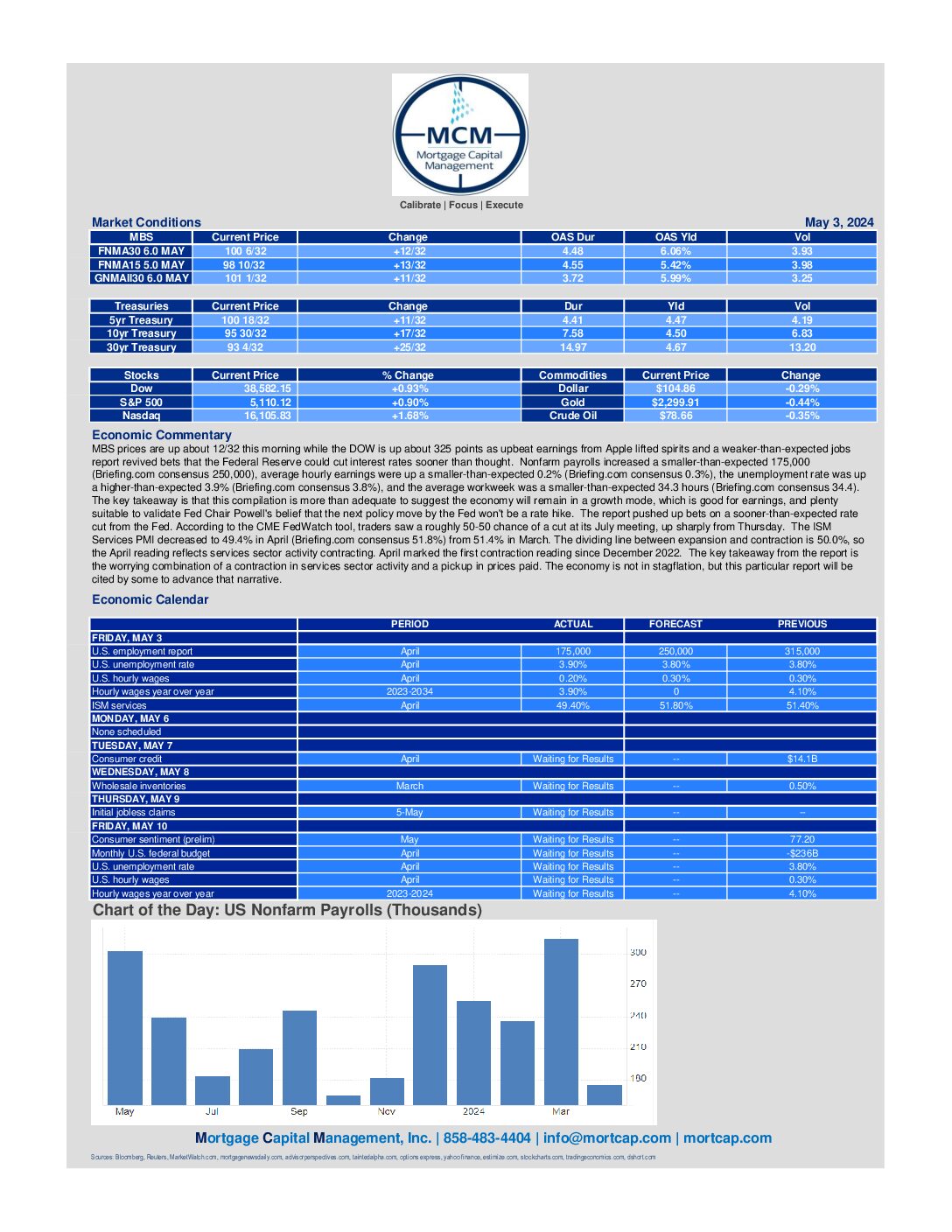

MBS prices are up about 12/32 this morning while the DOW is up about 325 points as upbeat earnings from Apple lifted spirits and a weaker-than-expected jobs report revived bets that the Federal Reserve could cut interest rates sooner than thought. Nonfarm payrolls increased a smaller-than-expected 175,000 (Briefing.com consensus

May 2nd Market Commentary

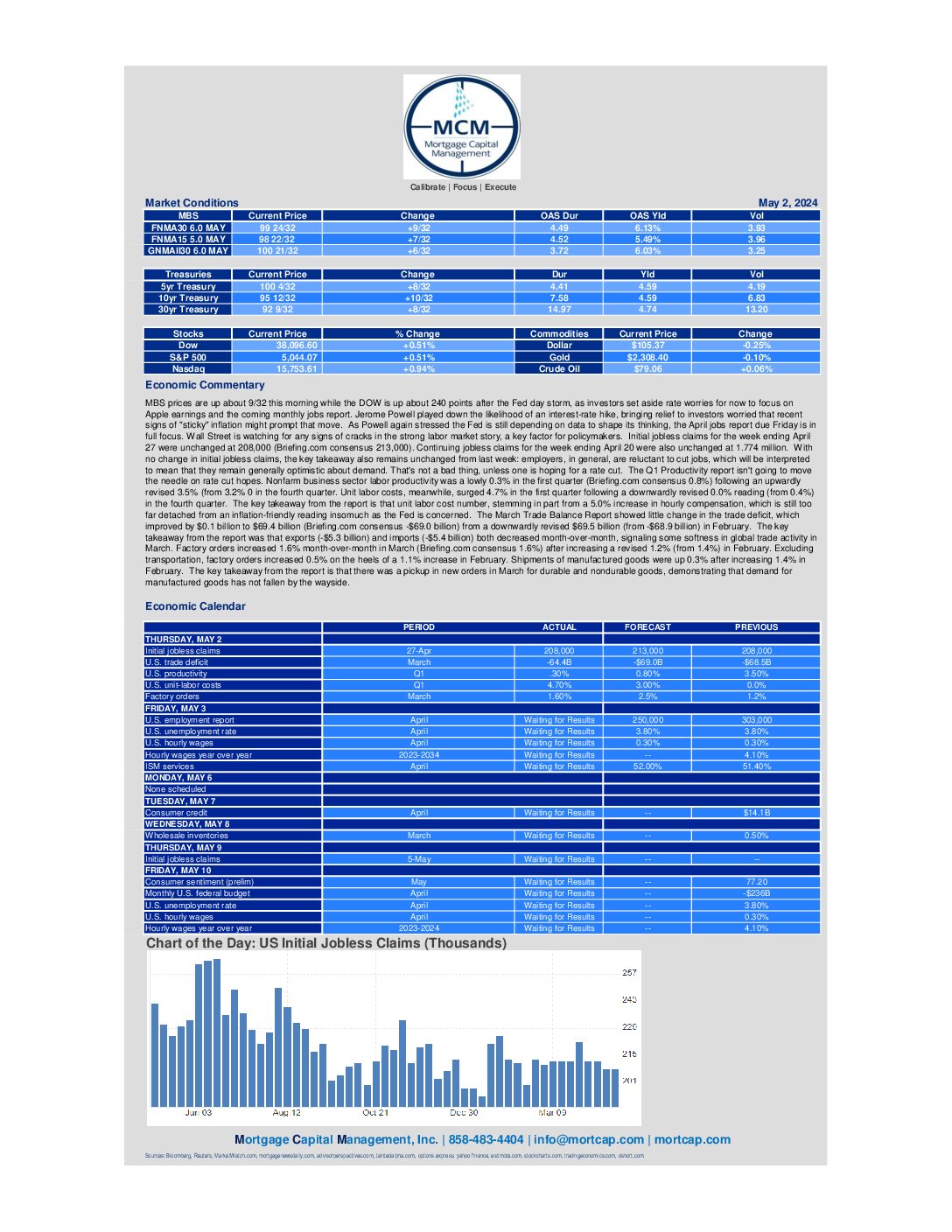

BS prices are up about 9/32 this morning while the DOW is up about 240 points after the Fed day storm, as investors set aside rate worries for now to focus on Apple earnings and the coming monthly jobs report. Jerome Powell played down the likelihood of an interest-rate hike,

May 1st Market Commentary

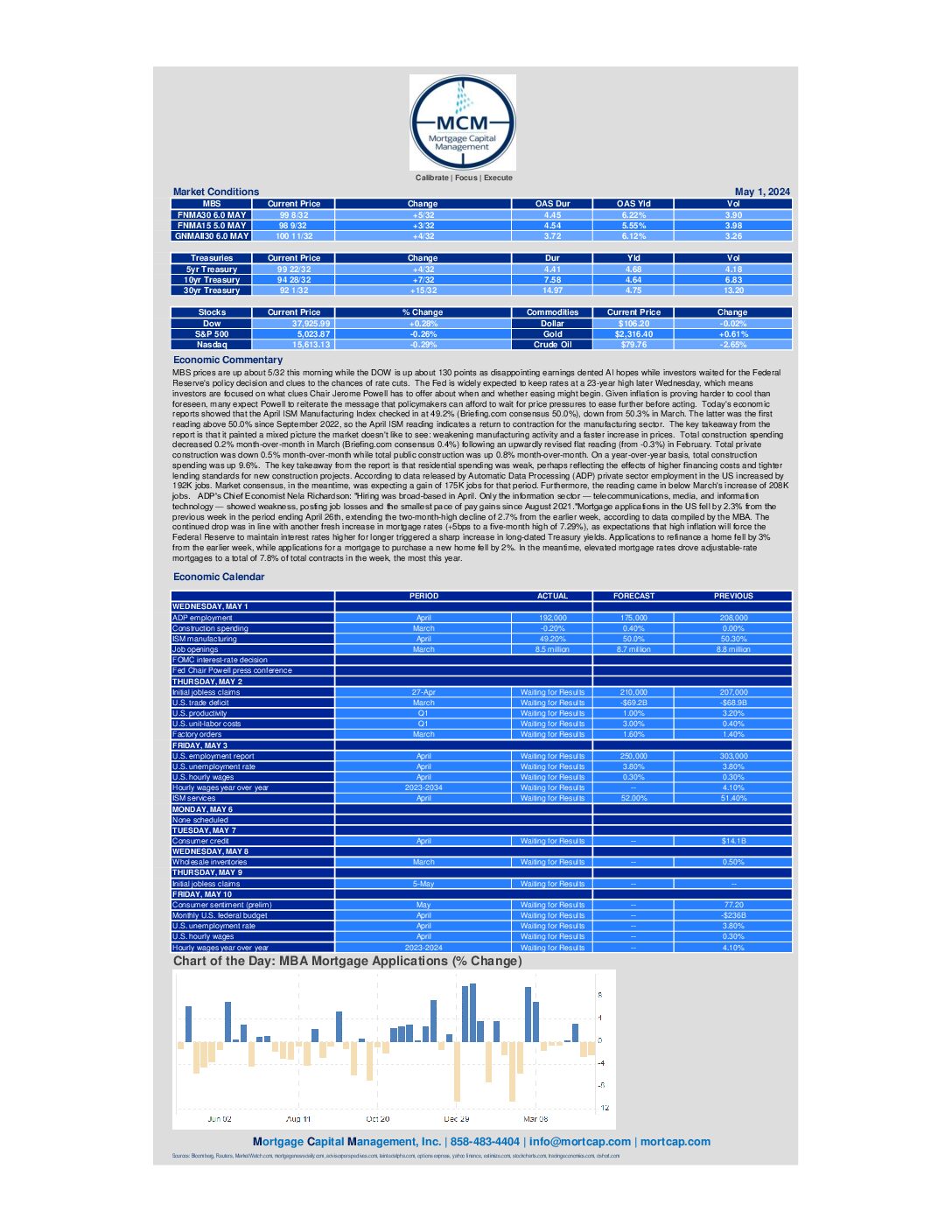

MBS prices are up about 5/32 this morning while the DOW is up about 130 points as disappointing earnings dented AI hopes while investors waited for the Federal Reserve's policy decision and clues to the chances of rate cuts. The Fed is widely expected to keep rates at a

April 30th Market Commentary

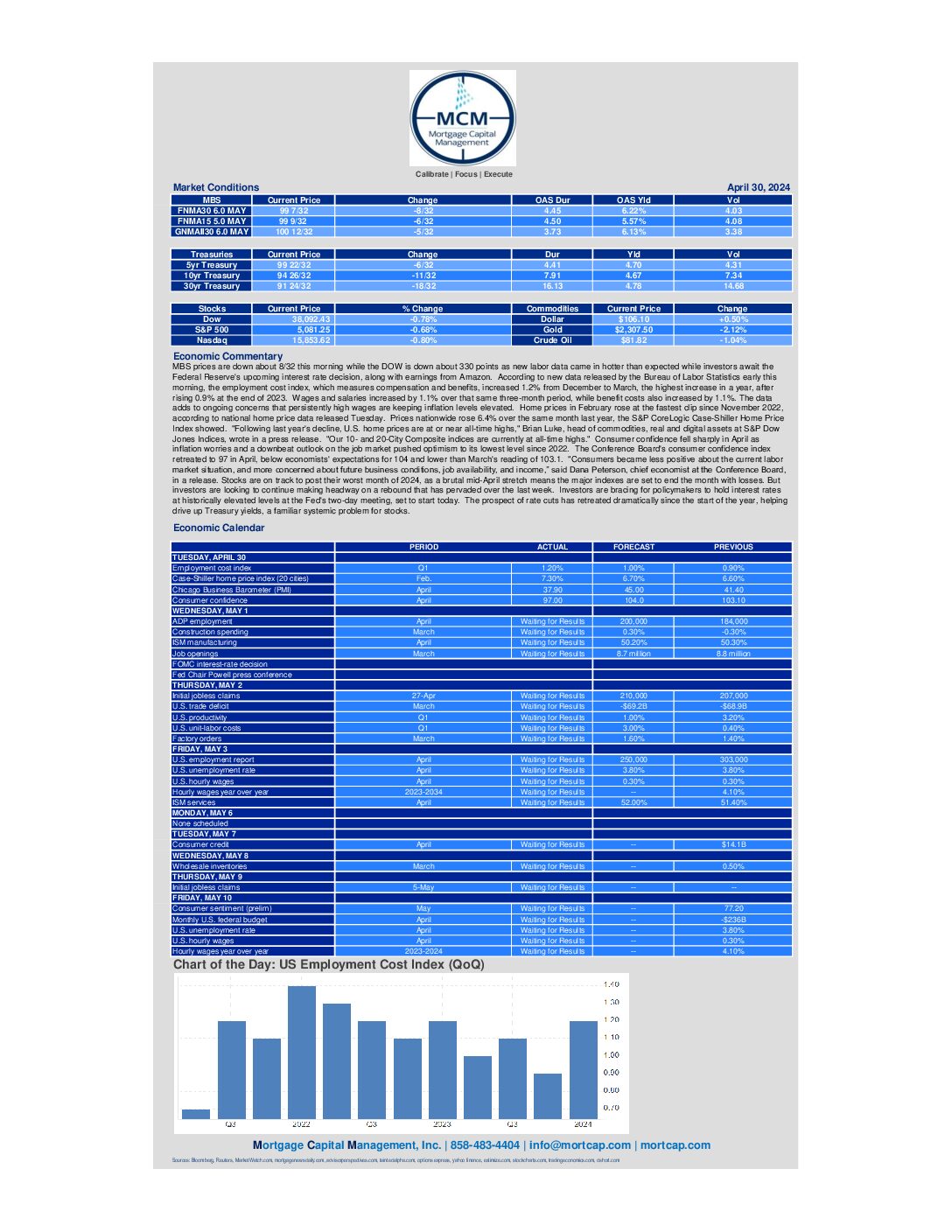

MBS prices are down about 8/32 this morning while the DOW is down about 330 points as new labor data came in hotter than expected while investors await the Federal Reserve's upcoming interest rate decision, along with earnings from Amazon. Investors are bracing for policymakers to hold interest

April 29th Market Commentary

MBS prices are up about 4/32 this morning while the DOW is up about 110 points to start a big week filled with a Federal Reserve rate decision, the monthly jobs report, and earnings from more "Magnificent Seven" tech heavyweights. In focus is whether Fed policymakers will backtrack

April 26th Market Commentary

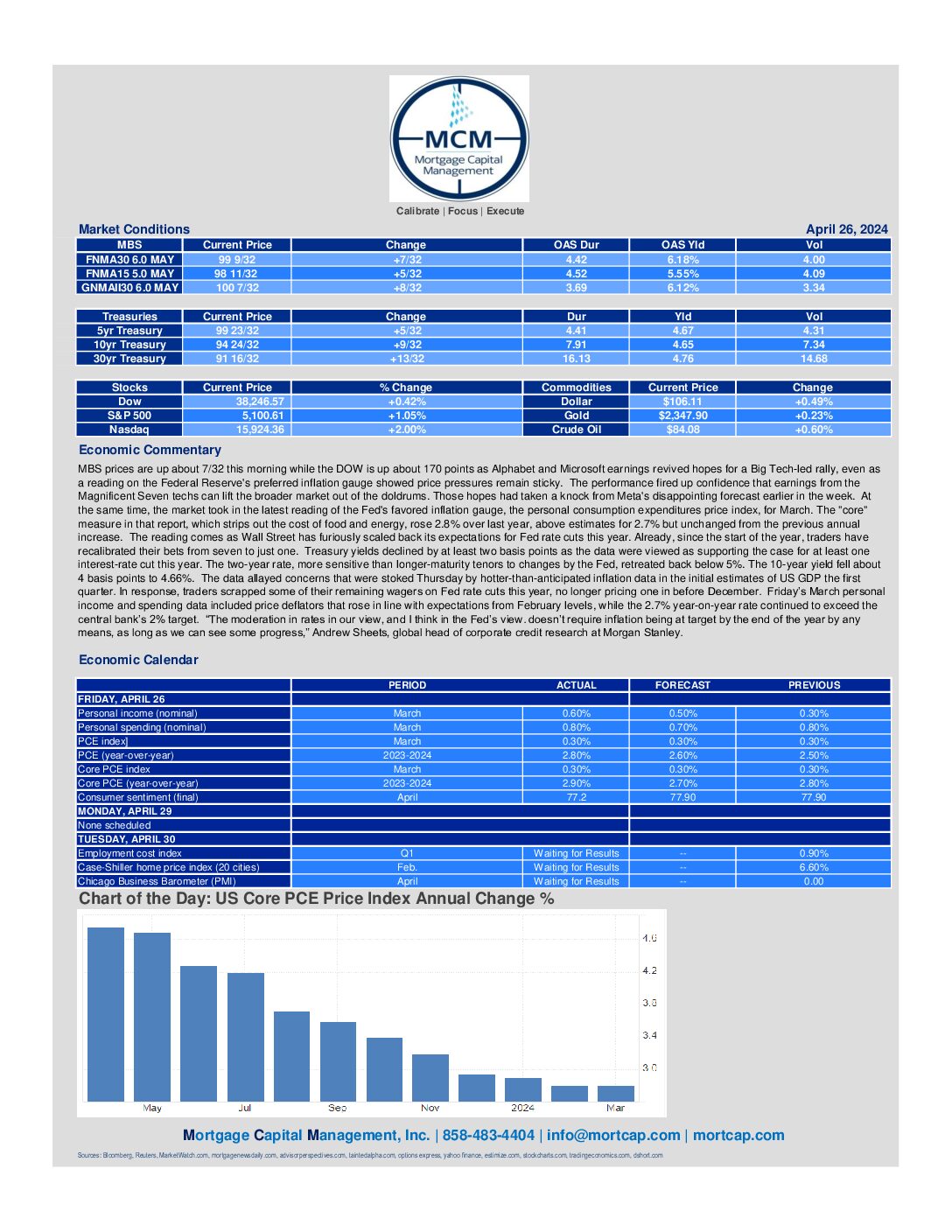

MBS prices are up about 7/32 this morning while the DOW is up about 170 points as Alphabet and Microsoft earnings revived hopes for a Big Tech-led rally, even as a reading on the Federal Reserve's preferred inflation gauge showed price pressures remain sticky. Treasury yields declined by

April 24th Market Commentary

MBS prices are down about 7/32 this morning while the DOW is down about 130 points as the ten year treasury yield rose 1.17% to 4.65. Mortgage applications in the US fell by 2.7% from the previous week in the period ending April 19th, trimming the 3.3% increase