FORWARD BUILDER COMMITMENTS

Forward builder commitments are very similar to our float down lock offering, but instead of providing spot commitments for the options required to lock a long rate on a single home, we allow a builder to provide rate lock assurance for an entire development.

This is an offering we pioneered and have been offering the industry since the 1980s. It was developed when our principal was working for a family real estate development business in Southern California. Interest rates were on the rise and homes were becoming less affordable by the time the construction was complete.

The innovation came in the form of the Float Down Lock for a one-time close on new construction. The offering provides assurance to the buyer that they’ll be able to afford the financing when the home is complete. Our Forward Builder Commitment makes this product available for a group of homes under construction.

Here is an example of how this product is used: A developer breaks ground on a $300 million project and expects about half of the homes to be financed through its own captive mortgage company while the other half will be financed by large, national lenders. The developer can buy an insurance option to hold rates to a certain level for the homes it plans to finance.

This is a much better option than just paying to buy down the rate because some investors, including the GSEs, have limitations on the resulting loan to value for the loans they buy. It’s far better to use a forward builder commitment to purchase an option and then hedge against it to mitigate any risk caused by rate volatility.

Like our popular float down locks, if the rates fall or don’t rise to the cap, the lower rate can be offered to the home buyer. Even if the rate goes higher, the borrower will pay only to the cap rate.

From a marketing perspective, this is a fantastic tool for construction lending as it offers buyers in a volatile market the assurance that they can afford the home under construction. We often refer to it as the builder’s rate protection plan. MCM helps lenders price the commitments and then hedge them appropriately during the timeframe in question.

In a market where mortgage interest rates are rising, offering new home buyers the security that comes with knowing what their financing will cost will save deals and help builders grow.

While builders see great value in this offering, it’s not something most companies can offer. MCM’s experience allows us to price the commitments properly and then hedge them correctly. One mistake we often see is a lender attempting to hedge the risk in $10 million worth of float down locks on a development by selling an equal amount for the TBA. If the market sells off, the lender will be successful, but if it rallies the lender will have too much TBA coverage while the hedged loans will fall out or close at lower rates.

When lenders see this happening, they will correct their hedging strategy, but in a volatile market they end up getting whipsawed back and forth, losing money on every trade. It’s far better to just buy an option to hedge based on good market intelligence and analytics, which MCM provides.

This service is often purchased as a stand-alone offering, but MCM also provides this service to clients working with us through either type of standard relationship

Partnership Account

MCM advises clients, who then execute trades, best execution based pooling and delivery. MCM is always available for conference calls to discuss trading strategies and to provide consulting and market analysis.

Guardian Account

MCM does it all, executing MBS trades, providing best execution based pooling and delivery, monitoring pricing and leading a daily client conference call to coordinate secondary marketing activities.

Under either type of business relationship, MCM’s systems, reporting and analysis tools are all available online providing instant accessibility to comprehensive analysis and reports, eliminating the need for the client to load, maintain and manage the software.

Ease of access, ease of use, quick report generation and real‑time “what‑if” scenarios all provide the client with the necessary tools to succeed in the world of risk management. Combined with MCM’s experienced advisors, Hedge Commander allows clients to grow and prosper in any market environment.

Since 1994, Mortgage Capital Management has helped mortgage bankers of every size become more profitable through the use of best-in-class pipeline risk management tools and strategiesy. Our pipeline risk management services, secondary marketing consulting, and hedging/trading services enable clients to prosper in any market environment.

For nearly 30 years, the U.S. mortgage industry has called upon Mortgage Capital Management for expert advice and proven technologies all designed to deliver best execution in service to a more profitable enterprise. Our customer list includes some of the most successful firms in the business.

Viewing the online demo costs you nothing and will shed light on a unique approach to secondary marketing success that you won’t find anywhere else. Don’t settle for mediocre when excellence is achievable.

Get the MCM Competitive Advantage! Call us to today to learn more or schedule an online demo: 858.483.4404 x220

Call us to today to learn more or schedule an online demo

Project & Services

May 8th Market Commentary

MBS prices are down about 3/32 this morning while the DOW is up about 85 points as investors tried to read the rate-cut runes and weighed a fresh batch of earnings reports for insight into the chance of a corporate America-spurred revival. Mortgage applications in the US rose

May 7th Market Commentary

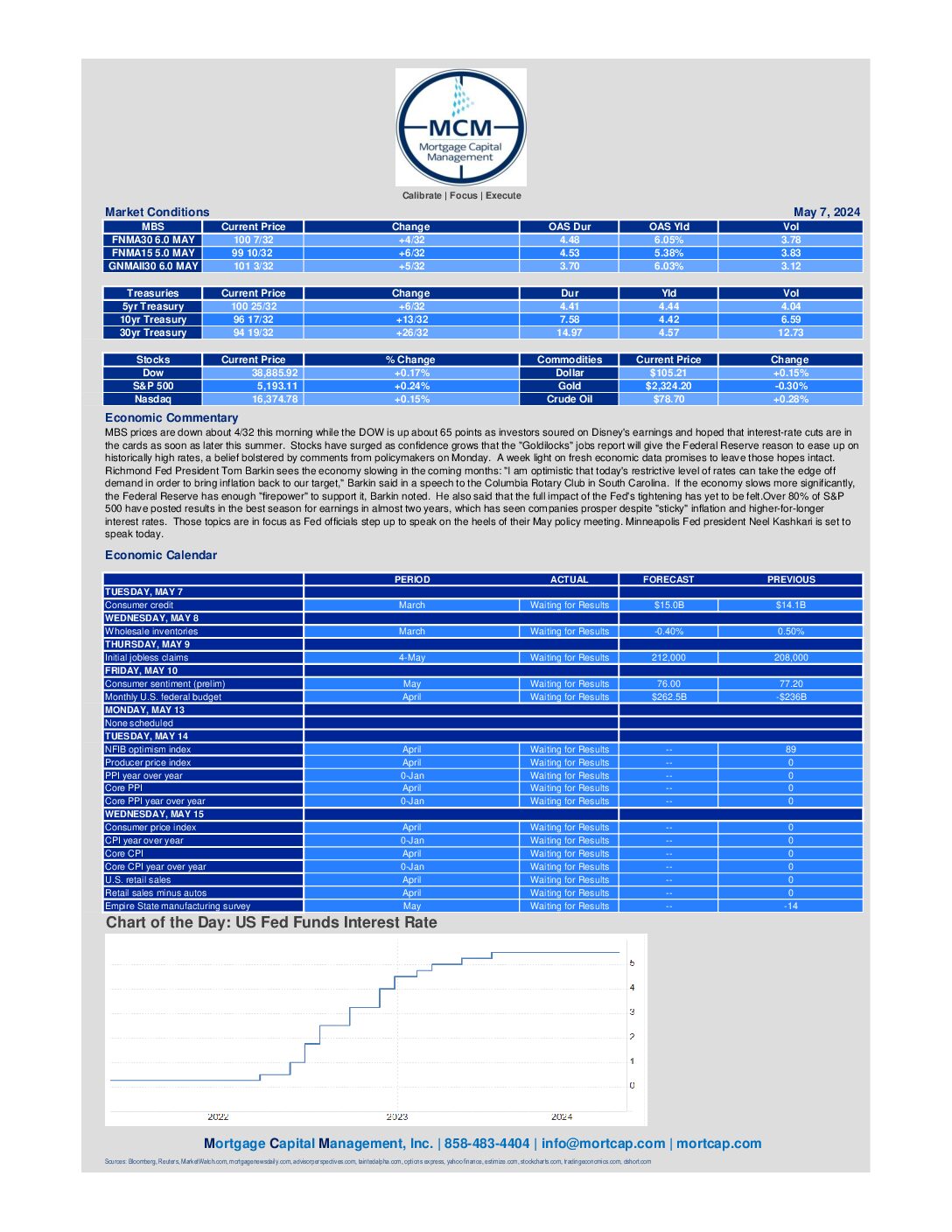

MBS prices are down about 4/32 this morning while the DOW is up about 65 points as investors soured on Disney's earnings and hoped that interest-rate cuts are in the cards as soon as later this summer. Richmond Fed President Tom Barkin sees the economy slowing in the coming

May 6th Market Commentary

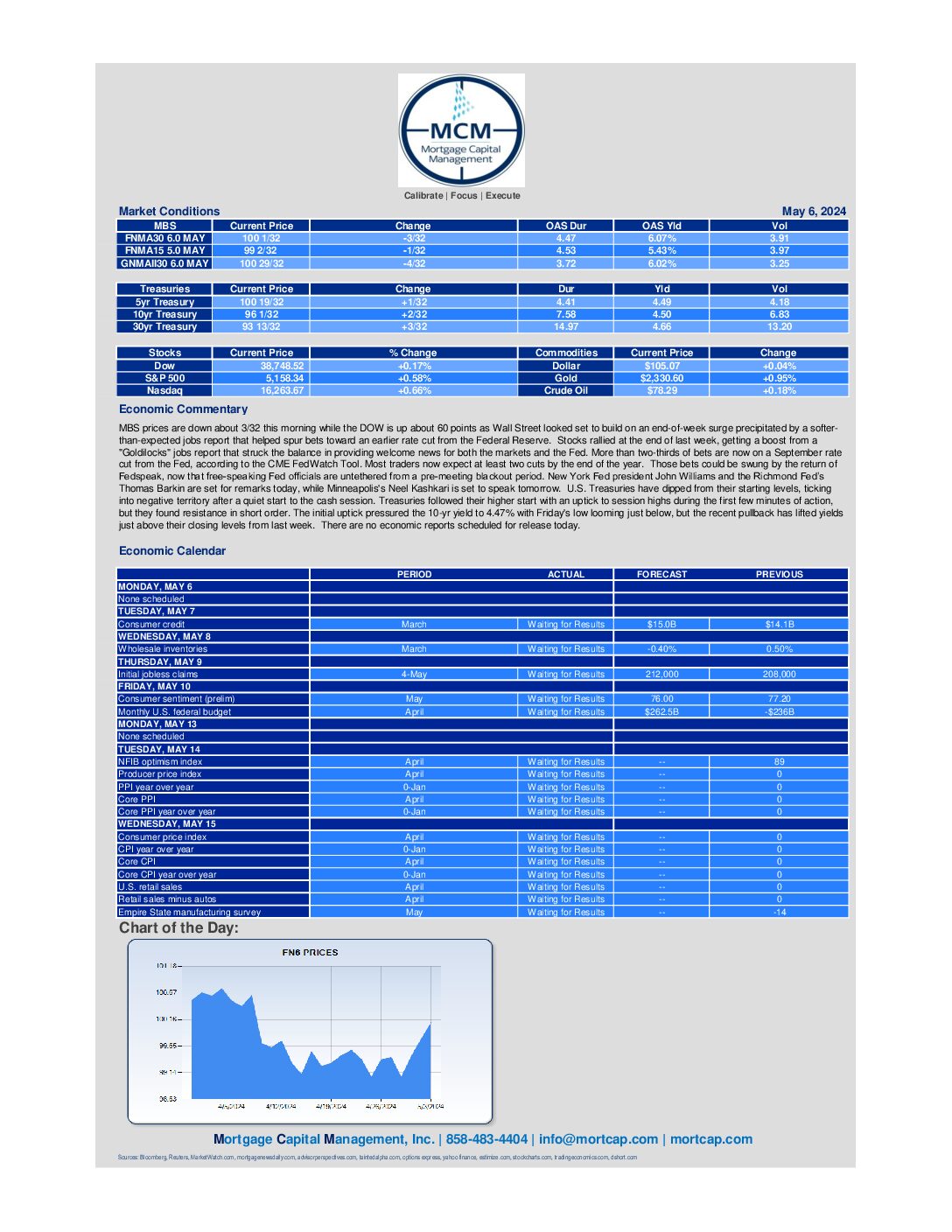

MBS prices are down about 3/32 this morning while the DOW is up about 60 points as Wall Street looked set to build on an end-of-week surge precipitated by a softer-than-expected jobs report that helped spur bets toward an earlier rate cut from the Federal Reserve. More than two-thirds

May 3rd Market Commentary

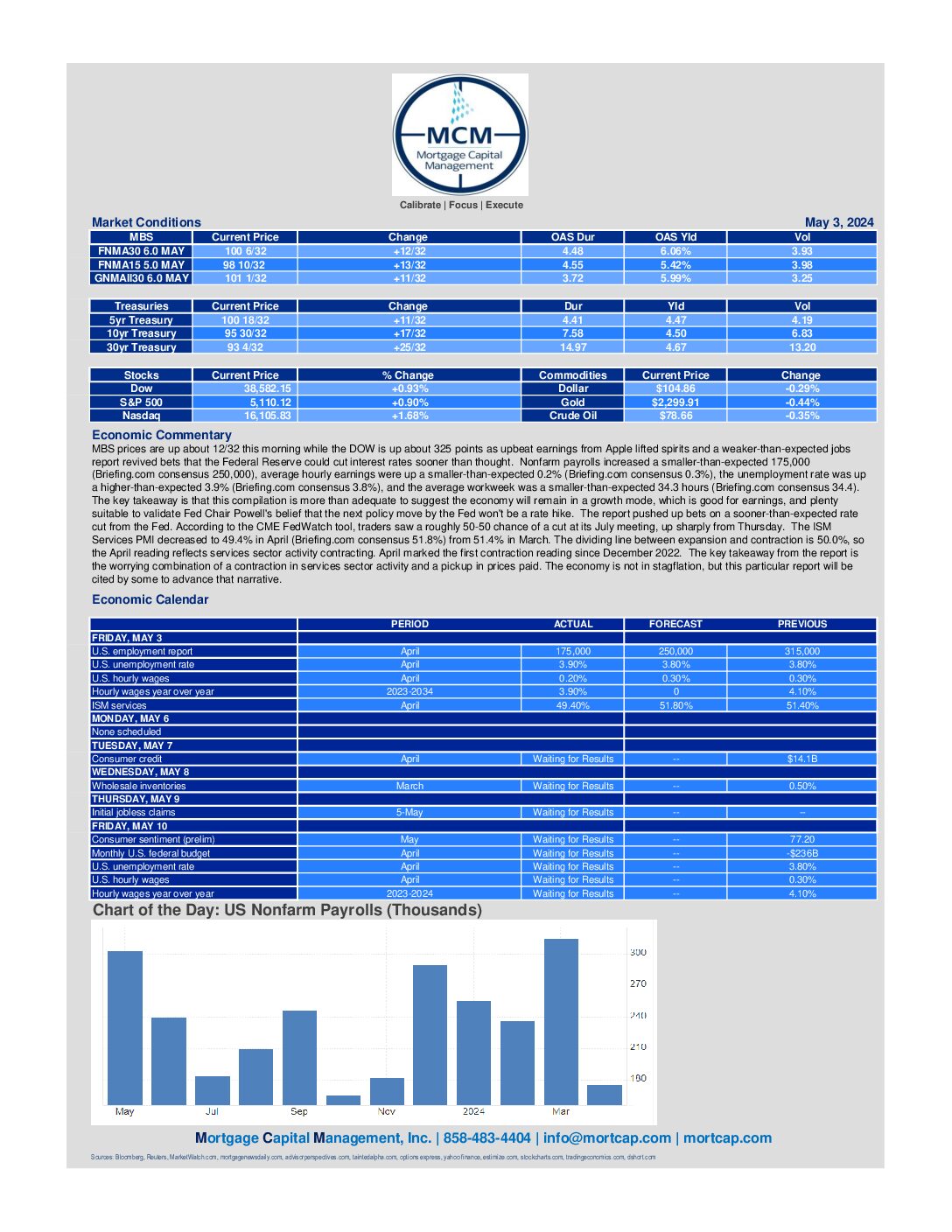

MBS prices are up about 12/32 this morning while the DOW is up about 325 points as upbeat earnings from Apple lifted spirits and a weaker-than-expected jobs report revived bets that the Federal Reserve could cut interest rates sooner than thought. Nonfarm payrolls increased a smaller-than-expected 175,000 (Briefing.com consensus

May 2nd Market Commentary

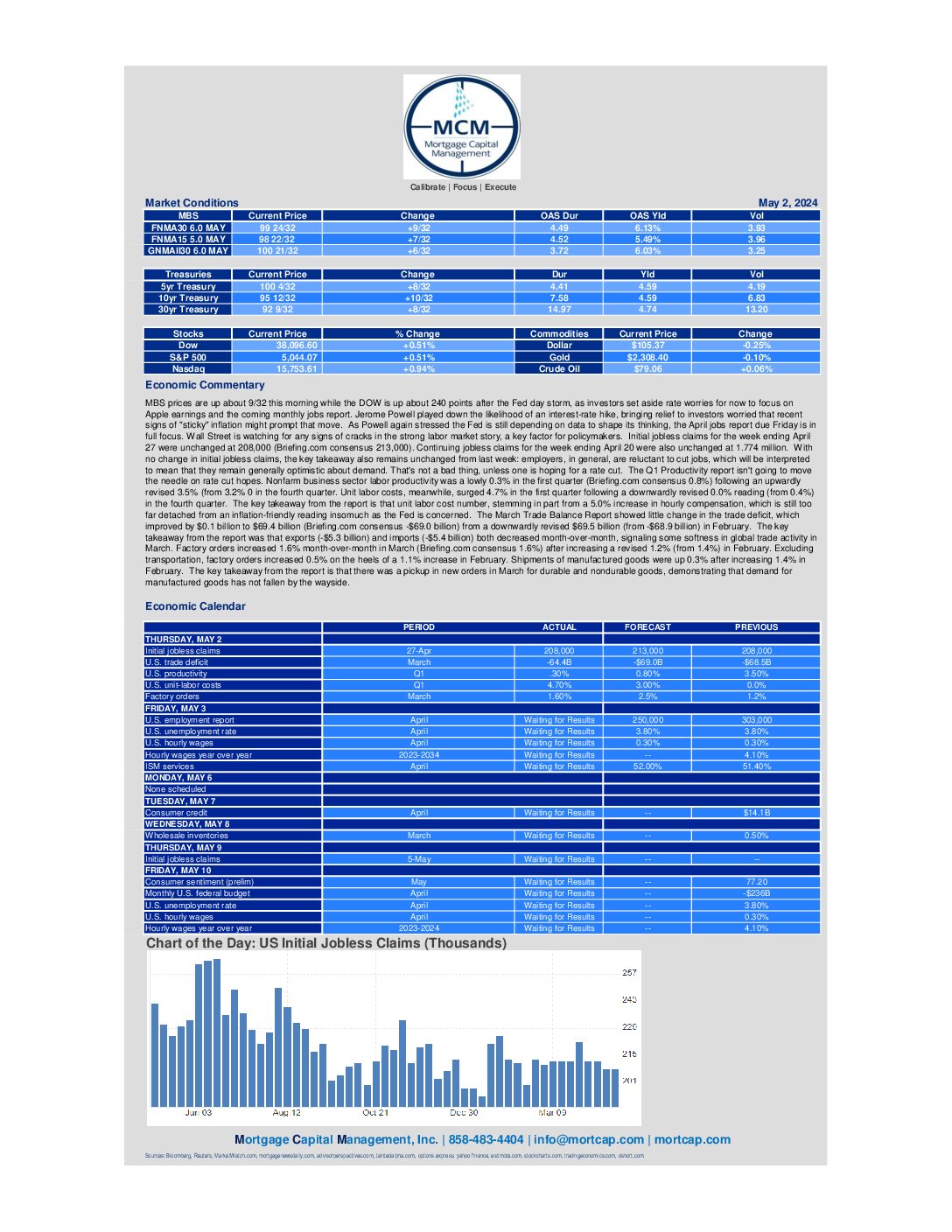

BS prices are up about 9/32 this morning while the DOW is up about 240 points after the Fed day storm, as investors set aside rate worries for now to focus on Apple earnings and the coming monthly jobs report. Jerome Powell played down the likelihood of an interest-rate hike,

May 1st Market Commentary

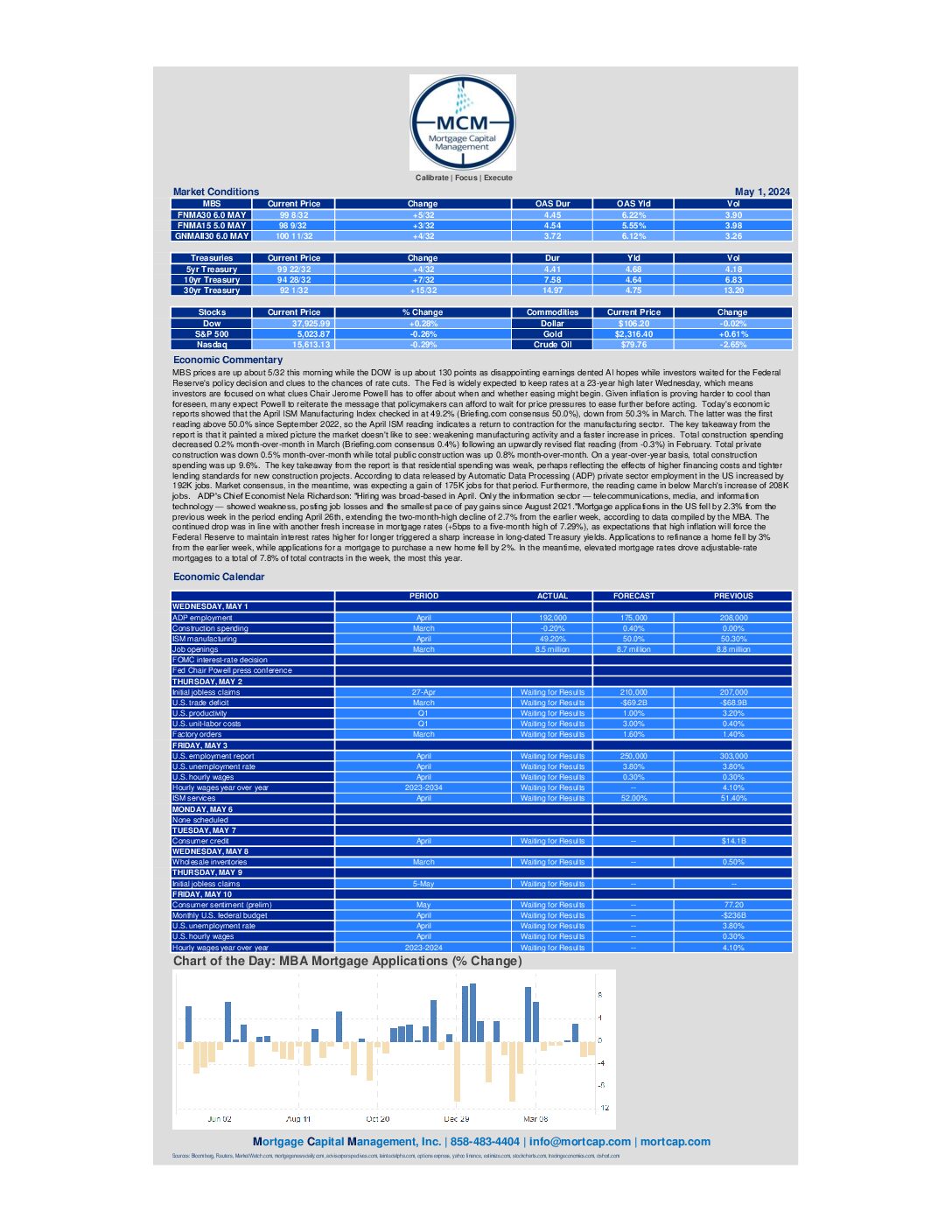

MBS prices are up about 5/32 this morning while the DOW is up about 130 points as disappointing earnings dented AI hopes while investors waited for the Federal Reserve's policy decision and clues to the chances of rate cuts. The Fed is widely expected to keep rates at a

April 30th Market Commentary

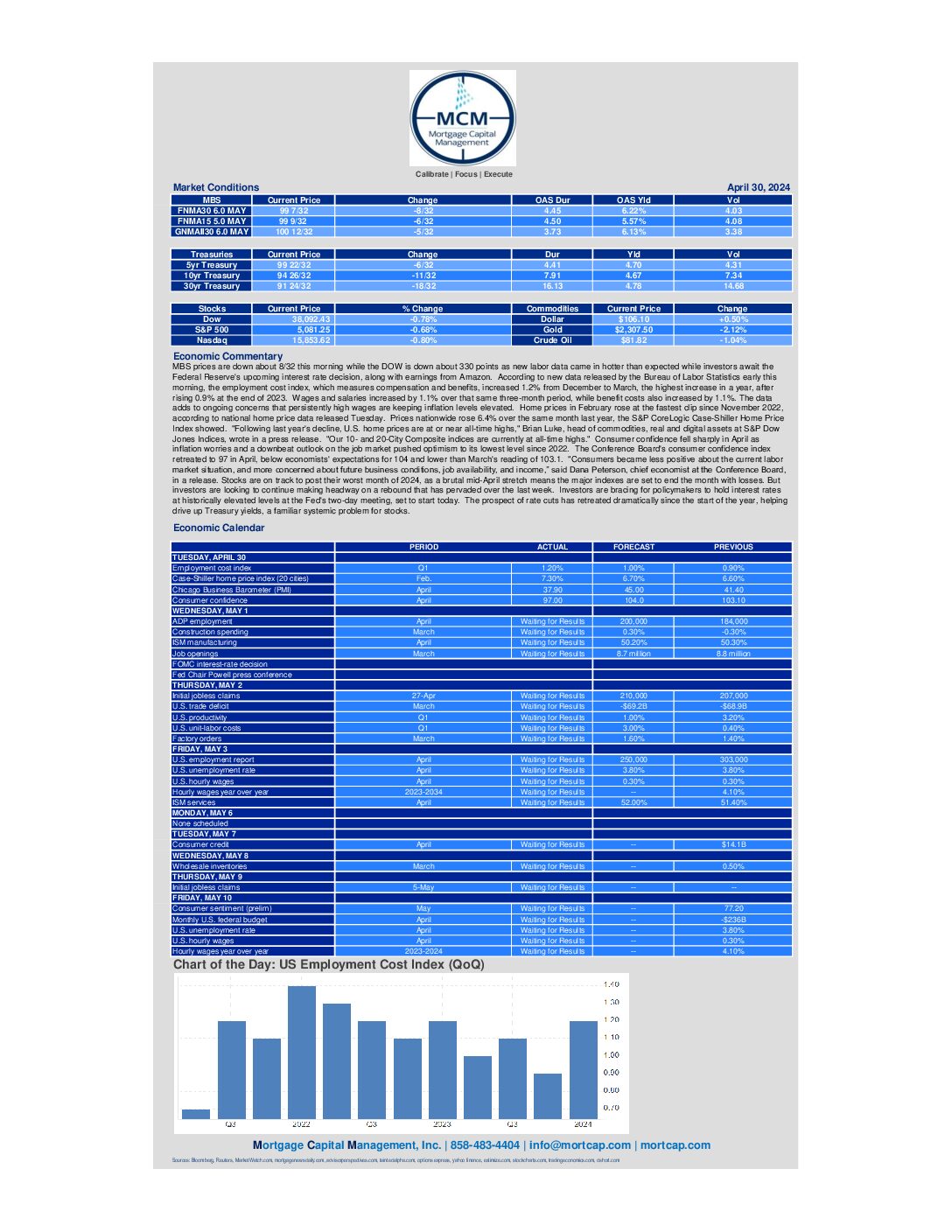

MBS prices are down about 8/32 this morning while the DOW is down about 330 points as new labor data came in hotter than expected while investors await the Federal Reserve's upcoming interest rate decision, along with earnings from Amazon. Investors are bracing for policymakers to hold interest

April 29th Market Commentary

MBS prices are up about 4/32 this morning while the DOW is up about 110 points to start a big week filled with a Federal Reserve rate decision, the monthly jobs report, and earnings from more "Magnificent Seven" tech heavyweights. In focus is whether Fed policymakers will backtrack

April 26th Market Commentary

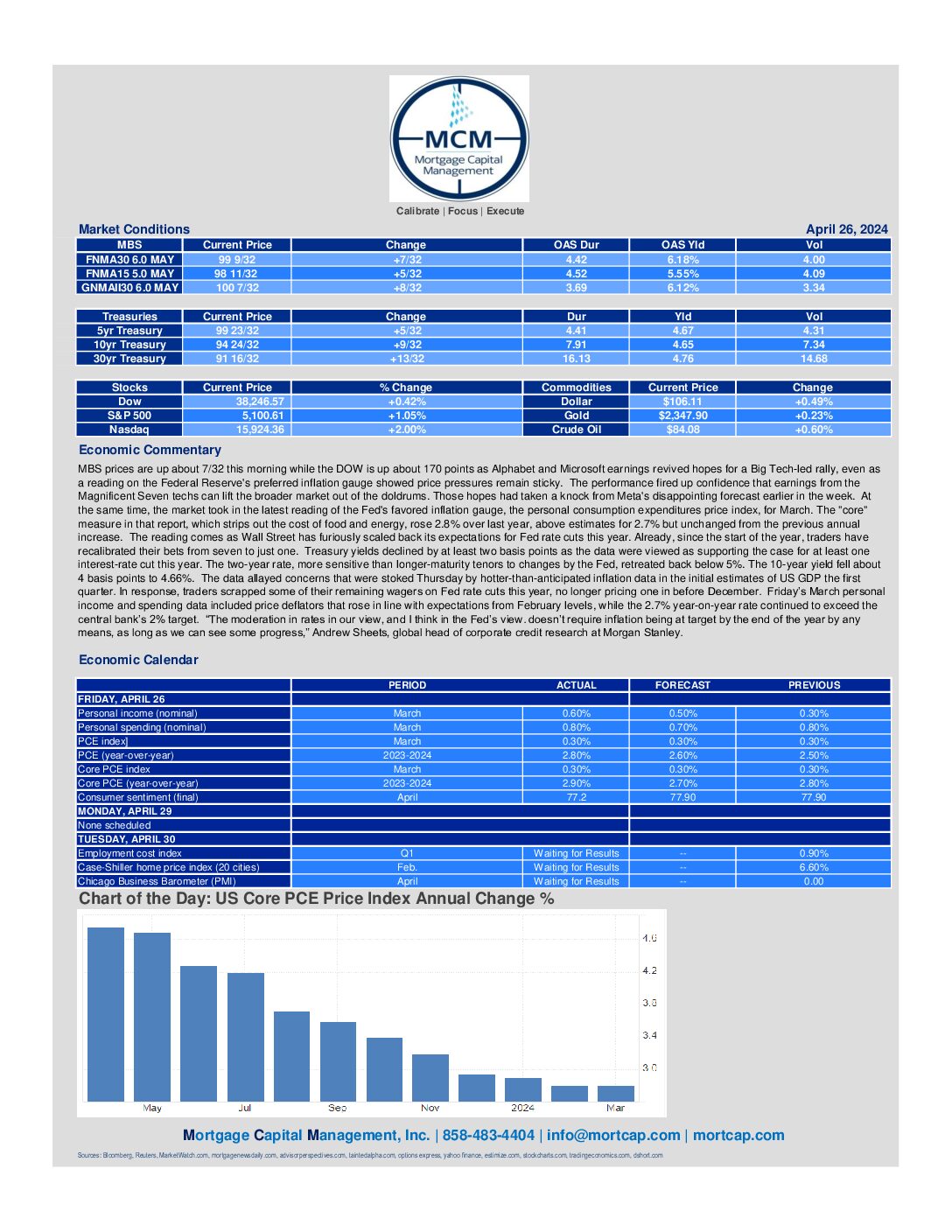

MBS prices are up about 7/32 this morning while the DOW is up about 170 points as Alphabet and Microsoft earnings revived hopes for a Big Tech-led rally, even as a reading on the Federal Reserve's preferred inflation gauge showed price pressures remain sticky. Treasury yields declined by

April 24th Market Commentary

MBS prices are down about 7/32 this morning while the DOW is down about 130 points as the ten year treasury yield rose 1.17% to 4.65. Mortgage applications in the US fell by 2.7% from the previous week in the period ending April 19th, trimming the 3.3% increase